- SOUN has posted negative net income every year from 2019 through 2025 — seven consecutive annual losses.

- FY 2025 operating cash flow: -$98.22M. Operations funded by $208.07M in equity financing, not revenue.

- CEO and CFO sold shares simultaneously in March 2026. Zero insider purchases in the same three-month window.

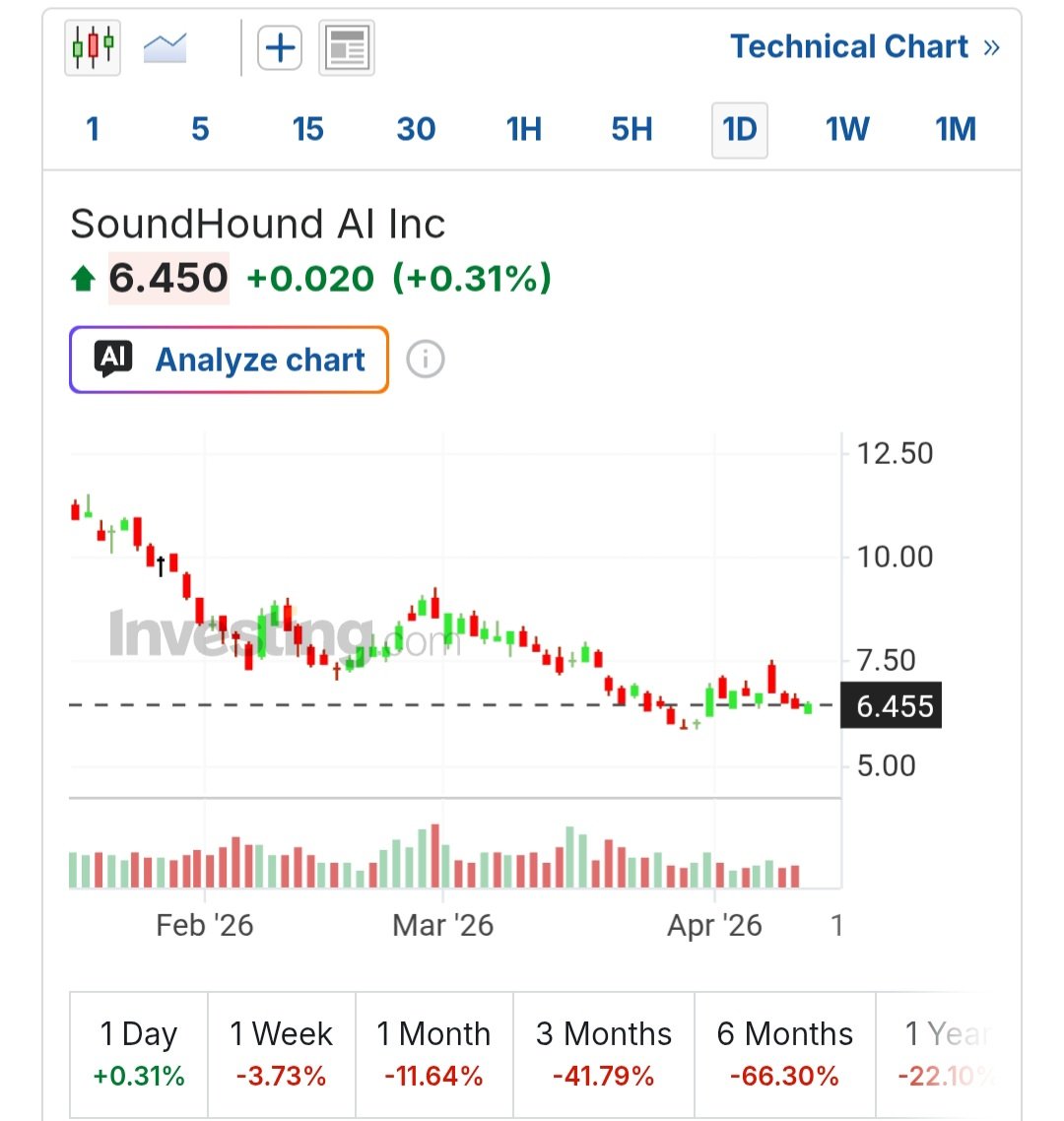

SOUN YTD: -35% | vs. 52-week high: -71%

Jim Cramer fielded a swing trade question on Mad Money about SoundHound AI (NASDAQ: SOUN) and gave a one-line verdict: they aren’t making money, so it’s a no. The data makes that hard to dispute.

SoundHound has run negative net income every single year since 2019. That is not a growth-stage company burning cash to capture a market — that is a pattern. FY 2025 revenue nearly doubled to $168.92M. The top line looks like a momentum story. Everything below it does not. Operating cash flow landed at -$98.22M. The company covered that gap with $208.07M in equity financing. Stock-based compensation consumed $80.6M of the full year on its own.

SOUN currently trades at $6.43, down roughly 35% year-to-date and 71% off its 52-week high of $22.17. The market is not pricing in a turnaround.

The bull case is not irrational on paper. Management issued 2026 revenue guidance of $225M to $260M. Sell-side consensus sits at a $14.62 price target — more than double the current price. If voice AI does become embedded infrastructure across automotive and restaurant verticals, and if SoundHound reaches cash-flow breakeven before the balance sheet forces another dilutive raise, the math can work.

The problem is the signal coming from inside the building. The CEO and CFO both sold shares in March 2026. No insider bought a single share in that same three-month window. Executives have access to the forward pipeline, the contract renewal rate, and the cash runway. They chose to sell. That does not confirm the bear case, but it does not support the bull case either.

The Nvidia association that briefly elevated retail interest in SOUN is dead. Nvidia divested its stake. The halo trade is over. What remains is a company that needs to demonstrate it can generate cash from operations — not from Wall Street — before the next equity raise resets the dilution clock again.

SoundHound has a real revenue growth story and zero proof it can monetize that growth into free cash flow. Seven years of losses funded by equity dilution is a structural problem, not a timing one. The $14.62 consensus price target is a ceiling that requires a profitability inflection — not a floor with embedded upside. Swing traders chasing 52-week lows here are betting on a catalyst that management has not delivered across multiple market cycles.

Watch Item: SOUN Q1 2026 earnings release — specifically operating cash flow and whether 2026 guidance midpoint of $242.5M holds. Any downward revision kills the bull case outright.

Disclaimer: This post is for informational purposes only and does not constitute investment advice. All investment decisions and their outcomes are solely the responsibility of the reader.