- Zeta Global pushed Athena to general availability March 24, opening it to all platform customers.

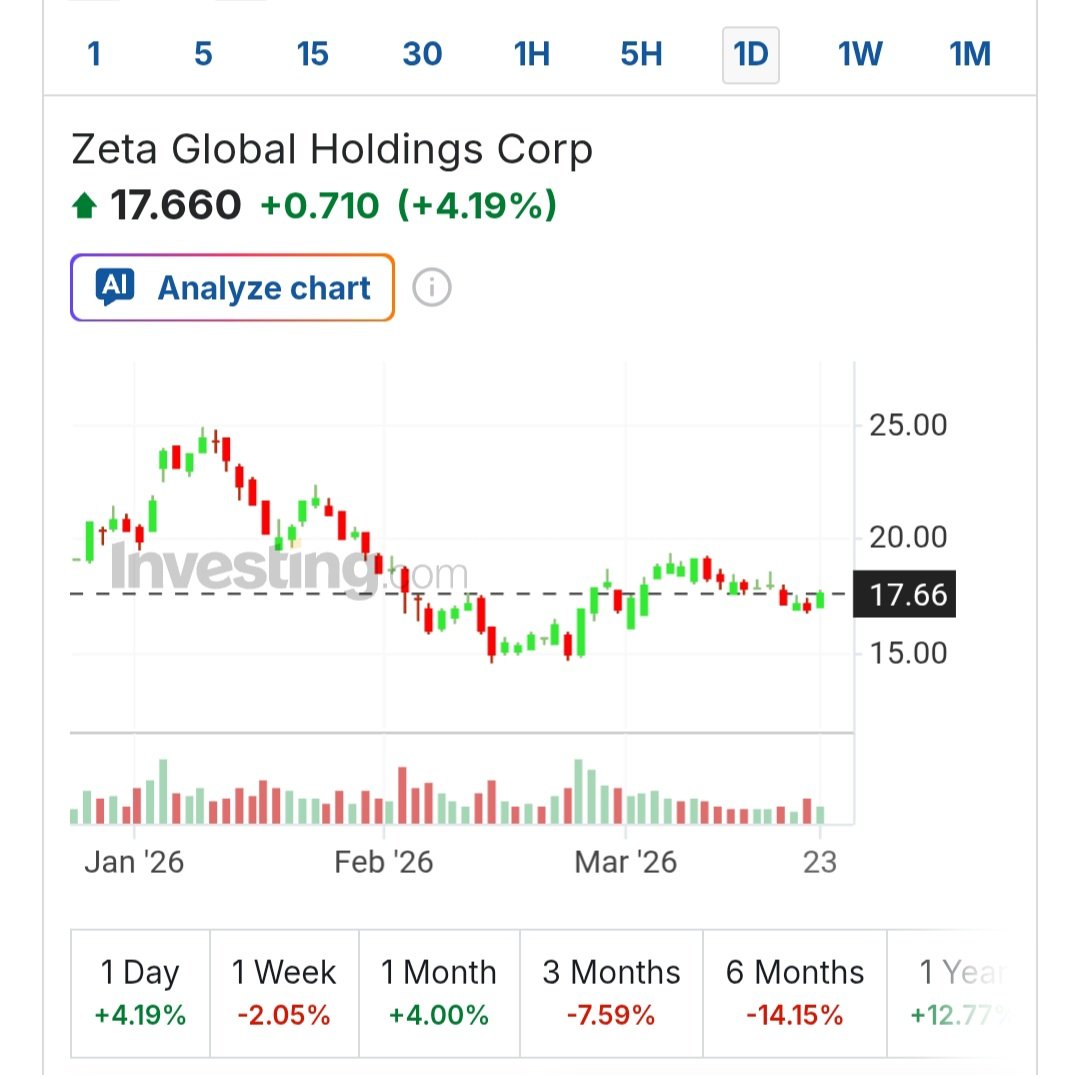

- Canaccord and DA Davidson hold Buy ratings; price targets at $30 and $29 vs. $17.66 current price.

- Revenue grew ~30% over the trailing twelve months; company not yet profitable but expected to turn this year.

Current Price: $17.66 (~41% discount to avg PT)

Athena is Zeta’s enterprise AI agent, now live for all Zeta Marketing Platform customers after a preview at Zeta Live in October 2025. It ships in two modules: Insights, a conversational analytics layer, and Advisor, a goal-based optimization tool. The system pulls from Zeta’s proprietary data cloud and identity graph and runs on OpenAI models under a partnership announced at CES 2026.

The operational claims are specific enough to take seriously. Early adopters reduced segmentation cycles from days to minutes and campaign execution from weeks to hours. Red Roof, a franchised lodging operator, is the named reference customer. Zeta reports clients see 6x return on ad spend across the platform broadly — Athena is positioned to extend that number, not establish it from scratch.

The OpenAI integration is the engine. The identity graph and data cloud are the moat argument. Steinberg’s point about proprietary data being non-replicable is the core bull thesis — and the claim Wall Street will spend the next several quarters stress-testing.

At $17.66, ZETA trades at a roughly 41% discount to the average sell-side price target of $29.50. That spread is not a rounding error — it reflects genuine disagreement about whether 30% revenue growth justifies the multiple on a company still burning cash at the operating line.

Both Canaccord Genuity and DA Davidson reiterated Buy ratings post-CES, citing the OpenAI partnership and Athena’s pull-forward timeline — originally slated for later in Q1 2026, now delivered on schedule. The market cap sits at $4.3 billion. Profitability, per consensus estimates, arrives sometime this calendar year. If that timing slips, the discount to price targets widens for the wrong reason.

The bull case is straightforward: a proprietary data asset, a credible enterprise product in GA, and a sell-side that sees 65%+ upside from current levels. The bear case is equally straightforward: pre-profitability SaaS with AI marketing competitors multiplying, and a stock that has already been cut in half from prior highs despite the product progress.

Athena’s GA release is a product milestone, not a financial event — it moves the narrative but not the income statement yet. The 6x ROAS figure is a platform-wide stat, not Athena-specific, and that distinction matters for modeling incremental revenue. Profitability is the single binary variable this year: hit it and the multiple re-rates, miss it and the discount to price targets becomes a trap. Two Buy-rated analysts at $29–$30 provide a ceiling reference, not a floor guarantee. The stock stays a show-me story until Q1 2026 earnings print with Athena customer attach data attached.

Watch Item: ZETA Q1 2026 earnings release — specifically Athena customer adoption figures, net revenue retention, and first operating profit confirmation.

Disclaimer: This post is for informational purposes only and does not constitute investment advice. All investment decisions and their outcomes are solely the responsibility of the reader.