- CFO Nitesh Sharan exits April 3; co-founder James Hom steps in as interim CFO.

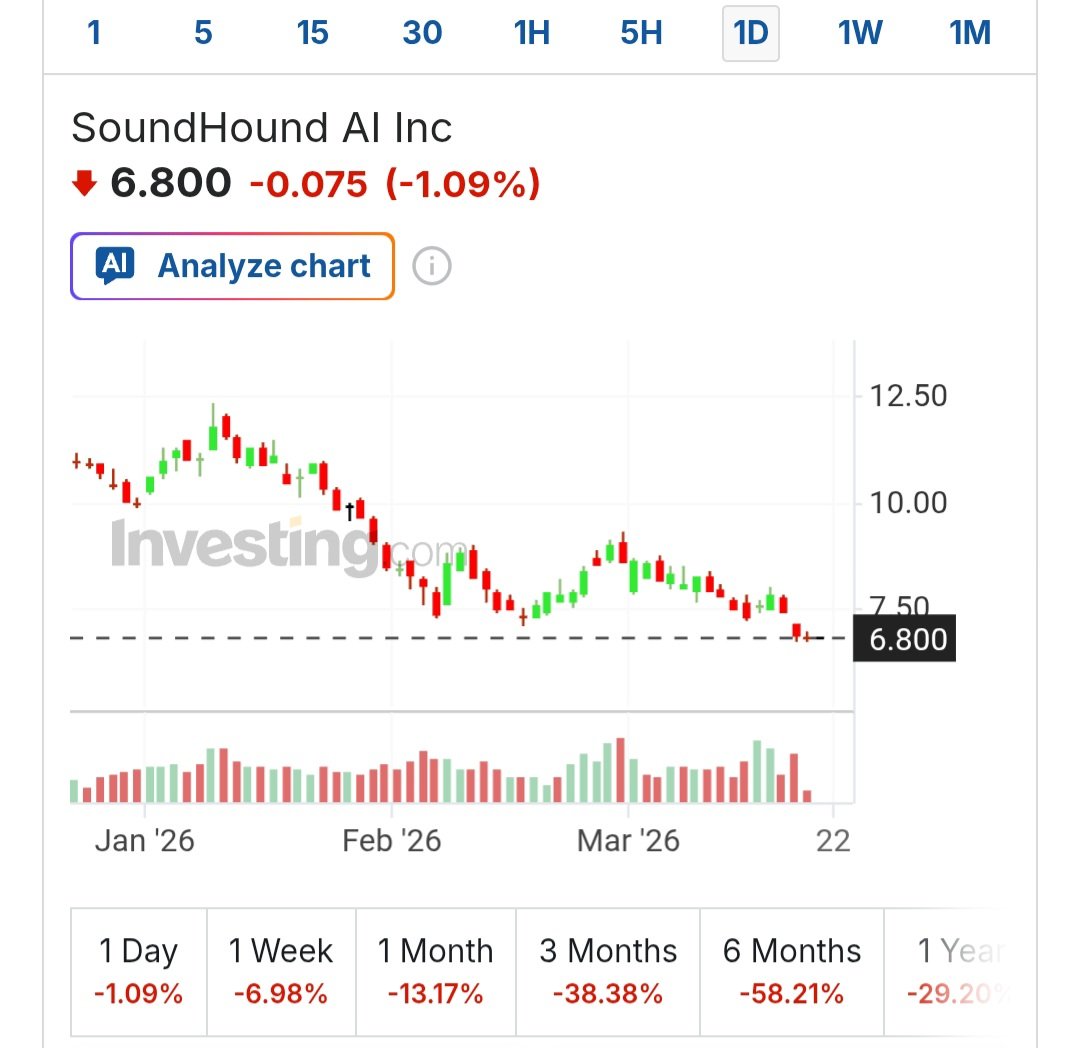

- SOUN fell 14% across two sessions; now trading 38% below its 100-day SMA.

- DA Davidson holds Buy, $14 target; consensus average sits at $14.50.

52-Wk Range: $6.52 – $22.17

SoundHound AI confirmed CFO Nitesh Sharan is leaving on April 3, 2026, to take a leadership role at a quantum computing firm. The company framed the exit as personal, with no link to disputes over financials or operations. Sharan will stay on as an advisor through the transition and says he intends to remain a long-term shareholder.

The market did not care about the diplomatic language. SOUN dropped 5.5% Wednesday when the news broke, then another 8.5% Thursday — closing near $6.76, just above its 52-week low of $6.52. Interim CFO duties fall to James Hom, co-founder and current Chief Product Officer. Hom held the CFO title from SoundHound’s founding in 2005 through the early years, so he is not walking in cold. A permanent search via executive recruiter is underway.

DA Davidson’s Gil Luria kept his Buy rating and $14 price target intact, calling the departure “disappointing” while dismissing any strategic read-through. The broader analyst picture mirrors that view — four Buys and one Hold over the past three months, with a $14.50 average target implying roughly 96% upside from current levels.

Luria did surface the structural concern that matters most: 30% of revenue concentrates in a single customer. A meaningful slice of total revenue is royalty-based — non-recurring by nature. That concentration risk does not disappear with a CFO change, and it does not improve with the stock near its floor.

Technicals offer no cover. SOUN trades 16% below its 20-day SMA and 38% below its 100-day SMA. RSI sits at 38.86. MACD prints at -0.3505, below the signal line. Key support is $6.50. Resistance is $8.00. The stock has lost 31% over the trailing twelve months.

A CFO exit alone rarely breaks a growth story. Here, it amplifies pre-existing concerns — single-customer revenue concentration, a non-recurring royalty model, and a stock already in a prolonged drawdown. Analyst price targets imply massive upside, but those targets require execution that has not shown up in the share price. The interim CFO arrangement buys time, not confidence. Until a permanent CFO is named and concentration risk is addressed, the path of least resistance stays downward.

Watch for the permanent CFO appointment and any Q1 2026 revenue update that addresses single-customer concentration — either event resets the narrative.

Disclaimer: This post is for informational purposes only and does not constitute investment advice. All investment decisions and their outcomes are solely the responsibility of the reader.