- SoundHound unveiled Agentic+, its first fully on-device multimodal automotive AI platform, at NVIDIA GTC.

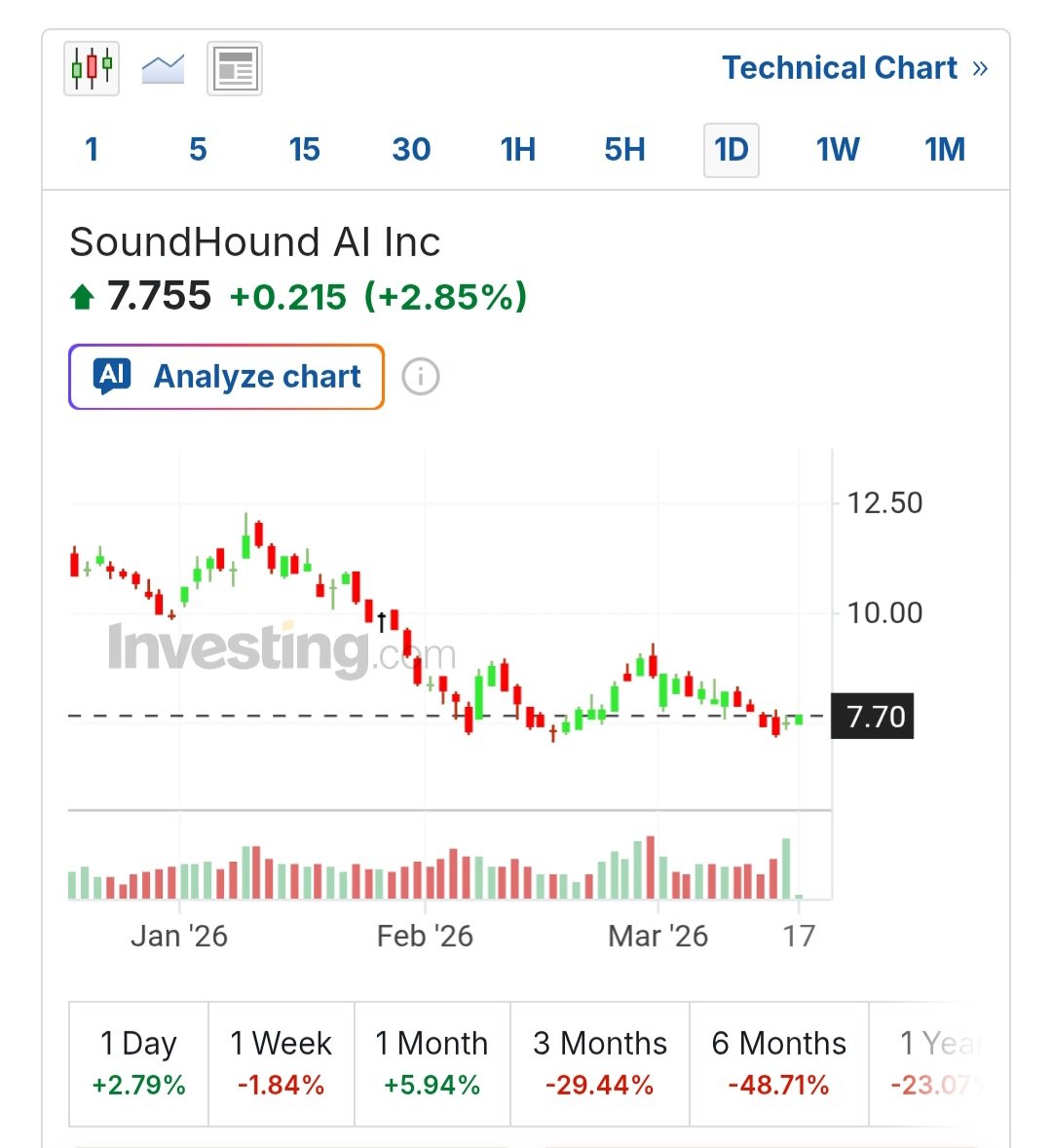

- SOUN trades at $7.54, down 28.9% YTD, with P/S at 18.89 and operating margin at -13.78%.

- Consensus price target is $14.63–$14.93; next binary event is Q1 2026 earnings on May 7.

YTD Return: -28.9%

SoundHound’s Agentic+ platform runs voice and vision AI entirely on-device, no cloud dependency. The pitch to OEMs is straightforward: lower latency, better data privacy, and connectivity-independent operation. For automakers evaluating cabin assistants for markets with unreliable data coverage, that is a real technical differentiator.

The NVIDIA GTC stage adds credibility optics. NVDA’s platform association gives SoundHound a marquee venue, and the multimodal framing — combining voice commands with visual context — moves the product beyond legacy voice-only implementations. That said, a demo is not a design win. The critical gap between a GTC keynote appearance and a production vehicle rollout is measured in years and OEM procurement cycles, not quarters.

Pre-market volume hit 44.5 million shares, roughly 1.72x the 30-day average of 25.7 million. Elevated participation confirms attention. It does not confirm conviction. RSI sat at 38.81 at the open — oversold territory, not a launching pad. The 50-day moving average at $9.11 and 200-day at $12.21 are both overhead resistance. Price needs a sustained close above $9.11 on volume to change the short-term technical narrative.

The financials do not support a comfortable entry at current multiples. P/S sits at 18.89, EV/Sales at 17.44, and price-to-book at 6.79. Free cash flow per share is -$0.18. Operating margin is -13.78%. The balance sheet provides some runway — current ratio of 4.59 and $0.60 cash per share — but dilution risk is real as losses persist.

The consensus analyst target of roughly $14.93 implies 98% upside from $7.54. That gap is not a buying signal by itself. It reflects the binary nature of SOUN’s story: if automotive design wins accelerate and revenue per share climbs materially from $0.40 TTM, the multiple re-rates. If adoption lags or hyperscalers bundle comparable functionality, the valuation compresses further. There is no middle-ground outcome priced into an 18x sales multiple on a loss-making company. The three-year return of 280.8% tells you this stock rewards early conviction — it also tells you timing matters enormously.

One structural positive: the on-device architecture is defensible against cloud-dependent competitors in specific use cases. Automakers have genuine reasons to prefer offline-capable systems. That is a niche, but it is a real one. Revenue confirmation from named OEM customers would be the first concrete evidence the strategy is converting.

SOUN stock is a speculative growth position, not an earnings compounder. The Agentic+ demo is technically credible and strategically logical, but it moves the valuation needle only if OEM contracts follow. At $7.54, the stock trades 48% below consensus — that discount reflects justified skepticism about the timeline from demo to production revenue, not a market pricing error. Position sizing should reflect the binary outcome profile. There is no floor argument built on current profitability.

Watch Item: Q1 2026 earnings on May 7, 2026 — specifically automotive revenue as a percentage of total revenue and any named OEM design win disclosures.

Disclaimer: This post is for informational purposes only and does not constitute investment advice. All investment decisions and their outcomes are solely the responsibility of the reader.