- SOUN lands first agentic AI platform deal with ACG, targeting Tier 2/3 telecom operators.

- Revenue grew nearly 100% in 2025; 2026 consensus loss estimate holds at $0.09/share.

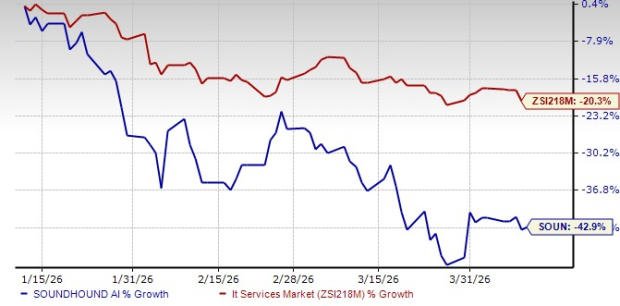

- Shares down 42.9% over three months; forward P/S at 11.3x, below the 12.0x industry average.

-42.9% — 3-Month Price Performance

SoundHound AI secured a partnership with Associated Carrier Group, making it the first vendor to deliver a full agentic AI platform to ACG’s member base of Tier 2 and Tier 3 telecom operators. That distinction matters. Large carriers already have entrenched vendor relationships. Mid-market operators don’t. That’s the opening.

The product itself is designed to do more than deflect calls. Agentic systems understand intent, pull live data, and close tickets autonomously — end-to-end. For operators drowning in call volume and squeezed on margins, first-call resolution rates and cost-per-interaction are the metrics that move EBITDA. SoundHound is selling directly into that pain point. The ACG channel accelerates distribution without requiring SOUN to win one carrier at a time.

This also changes the positioning narrative. SOUN is no longer pitching itself as a voice AI vendor. The ACG deal, layered on top of reported record enterprise deal counts in 2025, supports the case for a cross-vertical agentic platform. Telecom adds a recurring revenue profile that automotive and restaurant verticals alone don’t provide.

Microsoft’s Nuance integration gives large carriers a speech-AI stack bolted onto Azure compliance and enterprise sales relationships. That combination is hard to displace at the top of the market. LivePerson owns significant share in high-volume messaging and chat automation for mid-market telecoms. Neither is standing still.

SoundHound’s edge is specificity: full agentic resolution versus query routing. That’s a real technical differentiator today. Whether it holds as Microsoft accelerates Nuance development is the operative question for 2026.

On valuation, SOUN trades at 11.3x forward P/S — a discount to the 12.0x industry average. Given the stock’s 42.9% three-month decline against the sector’s 20.3% drop, the market is discounting execution risk aggressively. The 2026 consensus loss of $0.09/share is narrower than 2025’s $0.13, but profitability remains off the table near-term. Revenue growth at nearly 100% is the only number keeping the bull case alive. It has to keep printing.

The ACG deal is a legitimate strategic move, not a press release. Tier 2/3 telecom is an addressable market with real switching costs and recurring revenue potential. But SOUN’s stock has disconnected from its operating momentum, and that gap doesn’t close on partnership announcements alone. The path to re-rating runs through sustained revenue growth, gross margin improvement, and a credible timeline to cash flow breakeven. None of those are confirmed yet.

Watch Item: SOUN’s next earnings report — Q1 2025 revenue growth rate and any update to 2026 full-year revenue guidance. A deceleration below 70% growth kills the valuation thesis immediately.

Disclaimer: This post is for informational purposes only and does not constitute investment advice. All investment decisions and their outcomes are solely the responsibility of the reader.